The 50 30 20 Budget Rule with Budget Template

Are you ready to take control of your personal finances? Finding the right budgeting system can make all the difference. Today we’re talking about a tried-and-true method known as the 50/30/20 budget rule which is an incredibly versatile strategy for people of different incomes, financial goals, and lifestyles.

Table of Contents

ToggleThe best thing about this type of budgeting plan is that it’s fairly easy to understand and follow, so even if you’ve never used a budget before – no problem! To get started with this effective financial tool, just download our free printable template, and let’s dive into the basics.

What is the 50 30 20 Budget?

The 50 30 20 budget is a style of budgeting that breaks your spending and saving down into 3 simple categories. Each category is a certain percentage of your total after-tax income. Here are the categories.

50% into Needs

30% into Wants

20% into Saving/Debt Repayment

What is budgeting by percentage?

Budgeting by percentage is a fast and easy way to budget.

Instead of finding a spot for every dollar, you can quickly break your income down into different categories using percentages. This allows you to cut back on the amount of time it takes to set up your budget.

Why is the 50 30 20 Budget so Popular?

The 50 30 20 Budget has been a popular style of budgeting for many reasons. Let’s look at why this budget might be the right choice for you.

It works

The best thing about this budget is that it just plain works for most people. This budget works equally as well for people who consider themselves savers, as well as people who have gotten themself into too much debt and need help getting out.

For people who like to save, allowing 20% for savings should be a decent place to start building up their retirements. Much more than this and you may be taking money away from other important things like time spent with family.

For those that have lived paycheck to paycheck for far too long and have the credit card debt to show for it, the 50 30 20 budget is a great way to ‘stop the bleeding.’ By being forced to reduce your wants to 30% of your income, you should start to have more money to put toward debt repayment.

It is Simple

One of my favorite parts of the 50 30 20 budget is its simplicity. When someone asks my opinion on budgeting I will usually suggest the 50 30 20 plan as a great place to start.

Not only can I explain it in just a few moments, but the math is also simple enough for most people to do in their heads. What else could you ask for in a budget?

It is easy to stick with

One of my favorite parts of the 50 30 20 budget is its simplicity. When someone asks my opinion on budgeting I will usually suggest the 50 30 20 plan as a great place to start.

Not only can I explain it in just a few moments, but the math is also simple enough for most people to do in their heads. What else could you ask for in a budget?

Who is the 50 30 20 Budget For?

The 50 30 20 Budget plan can pretty much be utilized by anyone. From low earners to high earners, and spenders to savers, everyone will have something to gain from this flexible budget.

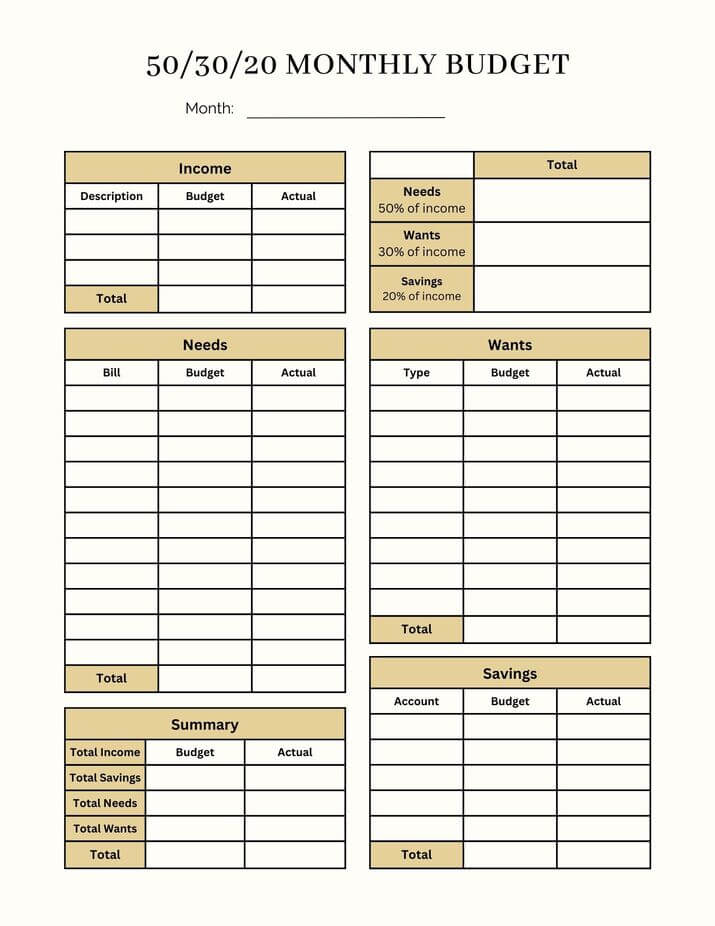

50 30 20 Budget Template

To help you get started with your new budget download my free 50 30 20 Budget Template. It’s nothing fancy, just lots of space to write down your expenses, what you budgeted for each category, and lastly what you spent for that category. It’s a simple way to keep track each month and should only take you a few minutes to complete.

How to use the 50 30 20 Rule to Make a Budget

Ok now that you know the what, why, and who, it’s time for the how. Let’s go through this together step by step, and see if we can get you on track with your budget.

First figure out your Income

The first step in any budget is figuring out how much you have to spend. This should be pretty simple but let’s go through some things to remember when you look at your income.

- The income should be your post-tax income (after taxes are taken out)

- Deductions like your 401k should be added back into your income as they will be added to your savings category

- Deductions like health insurance should also be added back into your income as they will go into the needs category

- If you get paid irregularly (like every 2 weeks) you need to consider how that will affect your budget. Check out my post on biweekly budgeting!

- If you don’t have a set amount of hours each week, do your best to find an average pay and go off of that as your income.

You can write your total income into the income section of the budget template.

50% going towards Needs

Now we are going to start with the needs category. This category accounts for 50% of your budget, and if you have overextended your budget, you may find this category gives you some trouble.

Here are some examples of things that will go into the needs category

- Mortgage/Rent

- Health Insurance Costs

- Insurance Premiums

- Groceries

- Utilities (Electric/Gas/Water)

- Travel expenses(Gas/Public Transportation)(not your car payment)

To calculate your wants category, grab a calculator and multiply your total income by 0.5, this is your total allowed for needs. Place that number in the upper right corner under the total section for needs.

Next fill out the income section of the budget template, including the “Bill Name” and how much you are budgeting for each.

Start by adding all the categories suggested above, and feel free to add any extra bills you can think of. Now add it all up and see what your total for the wants category adds up to!

How did you do with all of that? Are you having trouble fitting all of those expenses into 50% of your income? If so, you aren’t alone.

Do your best to find ways to cut back on those expenses. For those that are just barely over budget, making small changes like couponing, or shopping around for insurance could be all you need. But, if things are in really bad shape, you may have to do something as drastic as finding a new place to rent, or downsizing your home!

30% going towards Wants

The next category we have to look at is the wants category. This category will bring some people joy, and others will be haunted by the number of cuts they are going to need to make to their budget! A want is essentially anything you buy that is for entertainment or to make your life easier.

Here are a few examples of what goes in the wants category

- Car Payment

- Cell Phone Bill

- Dining Out

- Internet

- TV Cable or Streaming Services

- Traveling

- Gym Membership

- Any item that is a luxury and not a need

To calculate the total budget for the wants category, take your total income and multiply it by 0.3, and write that number in the upper right corner under wants.

Now just like the needs category, write down each want and how much you are budgeting. Add it all up and write the total down at the bottom.

How bad did that category hurt?

Not too bad? Good, as long as you aren’t a shopaholic, and can keep your spending in check, 30% of your income should be a reasonable amount to spend on wants. Now let’s move on to the section some look at with dread… Saving!

20% going toward Savings

Saving… you either love it, or you hate it. In my humble opinion, there are two types of people in the world when it comes to saving money.

- People who see money as a vehicle to purchase things.

- People who see money as a source of security.

There is no right or wrong mentality, it is just good to know where you generally sit. This is why I appreciate the 20% rule so much. It’s a great middle-ground for people who hate to save and may be drowning in debt, and for those people who tend to over-save and forget to enjoy life a little.

Now let’s look at some things that would count as saving categories in my view.

- Involuntary retirement saving accounts (401k, IRA, 403b)

- Saving for a downpayment on a home

- Emergency Fund

- Paying down debt

- Extra payment on the mortgage

- Extra payment on a vehicle

Some may disagree with me that paying down debt or paying extra on a vehicle would be considered saving. My response to that would be that as long as you are using debt repayment as a way to get out, and stay out of debt you are in good shape.

If you can pay down your credit cards now, so that you can start to save more in the near future, then I see no harm in it. You don’t want to be stuck in a debt cycle forever, and the best way to get out of debt is to do so as fast as possible!

Making large payments on your debts helps you to stay motivated, as you can easily see progress towards your goals much more quickly.

Finally, just like for the previous two categories, let’s fill out our budget planner. First, multiply your total income by 0.2 to find the total amount you should be saving per month. Write that in the upper right corner under savings.

Next, write down the type of account you have, and how much you are budgeting for each. Finally total up all your savings and write it at the bottom of the savings table under the total.

Finish up your Budgeting Template

Ok, now that you have all of your expenses added up, you can transfer each total down to the bottom left of the budgeting template.

There is a spot to write down how much you budgeted, as well as how much you actually spent. This will make it easy to see exactly where you stand with your new monthly budget.

Conclusion

And that’s it! You now have all the information you need to create your very own budget plan using the 50 30 20 rule. Remember, it’s all about finding a balance that works for you and your unique financial situation. Whether you’re just starting or looking to make some changes to your current budget, the 50 30 20 plan is a great way to get started. And with our free budget template, you can get started right away. So what are you waiting for? Start budgeting like a pro and take control of your finances today!

2 Comments