The 30-30-30-10 Budget – The best budget for beginners

When it comes to budgeting, there are a lot of different philosophies and strategies floating around out there. One you may have not heard of – and one that is a great budget for beginners is the 30 30 30 10 budget.

Table of Contents

ToggleIn this post, we’ll explore what this type of budget method is, how it works, and whether or not it will help you reach your financial goals. Ready to learn more? Let’s dive in!

What is the 30 30 30 10 Budget Rule?

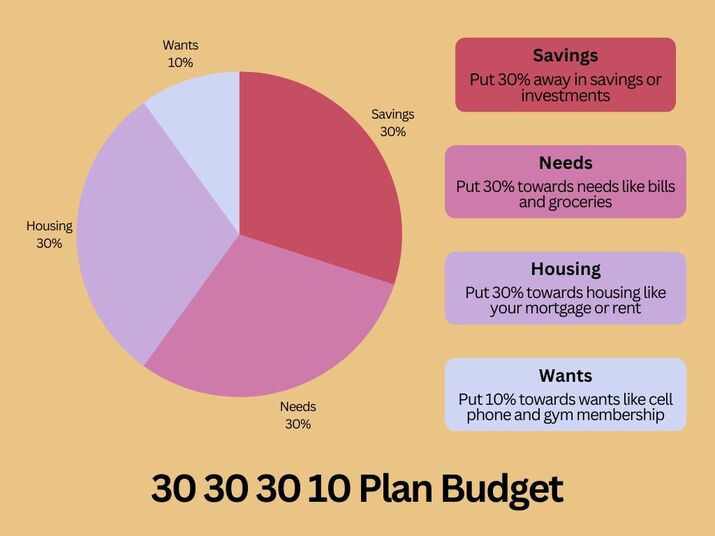

The 30 30 30 10 budget rule is a guideline for budgeting the percentage of your income that should go towards different expenses. Your expenses get broken down into four categories. Let’s take a quick look at the spending categories.

According to the rule, the first 30% goes towards the cost of housing, including your mortgage or rent. The second 30% of your income should go towards necessary spending like utilities and other housing expenses. The next 30% should be going towards saving money or debt repayment. Finally, the last 10% is your fun money, going towards your wants.

A great budget for beginner budgeters

While the 30 30 30 10 budget is a great budgeting method for those who have never budgeted before. It’s a simple, straightforward system for anyone who is just starting with budgeting. It provides ample amounts of spending for needs and wants.

Great for those living paycheck to paycheck

With the 30 30 30 10 budget you won’t have to make huge adjustments in your spending if you are already living paycheck to paycheck. The point of a budget is to give each dollar a home so that you don’t stray and put yourself in a tough spot. If you are looking for a more advanced budget that will all but guarantee reaching your financial goals, check out the 60 30 10 rule budget.

Before you spend one more single dollar, improve your finances first. You can start today by reviewing your spending habits, reducing credit card debt, and starting an emergency savings account.

The 30 30 30 10 Budget Breakdown

- Housing – 30 % of your income to mortgage or rent

- Needs – 30% of your income towards bills, groceries, etc.

- Savings – 30% of your income to saving, investing, and debt payoff

- Wants – 10% of your income to wants like cell phone, gym membership, or other discretionary spending

Why percentage-based budget plans?

When it comes to budgeting methods, using percentages isn’t the only budgeting rule you can use, though it may be the simplest. When using percentages you can just plug in numbers and go.

With zero-based budgeting, you have to go through every part of the budget until each dollar has a place. This can be time-consuming and also deter you from starting and managing your budget plan.

The amount of time it takes to budget is one of the biggest deterrents for most people. That’s what makes percentage base budgets so appealing. If the 30 30 30 10 budgeting rule doesn’t work for you check out the 50 30 20 budgeting strategy. This is a more user-friendly budgeting style for the average person.

Spend 30% of your Budget on Housing

When it comes to your budget, housing costs such as mortgage or rent most certainly play a major part. To ensure you stay on track with your financial goals it is recommended that you should aim to spend around 30% of your budget on housing-related expenses each month.

When you look at your rent or mortgage as a whole, it can seem overwhelming. However, when broken down into smaller amounts over the course of each month, this cost will be much more manageable for those who wish to maximize their money!

Spend 30% of your Budget on Savings

If you’re like most people, the thought of saving 30% of your income probably sounds about as appealing as getting a root canal. But according to some experts, that’s exactly what you should be doing if you want to retire early.

Of course, for low earners or high spenders, this may seem like an impossible feat. However, if you want to make this budget work, you are going to have to make some heavy cuts in spending.

A Few Examples Of Things That Would Go Into The Savings Category

- Retirement accounts

- Investing accounts

- College savings account

- Save money for a down payment on a house

- Real estate investments

- Emergency Fund

- Student Loan Debt

- Other House Expenses

Spend 30% of your Budget on Needs

Since we are putting so much of our monthly household income into savings, this means we won’t have as much left over for monthly needs. Let’s see how much goes into the needs category and if you’ll have enough monthly income to handle this budgeting method.

A Few Examples Of Things That Would Go In The Needs Category

- Utility Bills

- Insurance

- Groceries

- Health Care

- Child Support

- Other necessary expenses

- Maintenance costs

If you can keep your needs at or under 30% congratulations you are killing it! The last section, covering unnecessary spending, is all that is standing between you and financial independence!

Spend 10% of your Budget on Wants

The last section of the 30 30 30 10 budget is the “spending money” or wants category. This category covers all your expenses not covered under the previous three categories. Only lower-income earners or the big spenders should have trouble with this budget category,

A Few Examples Of Things That Would Go In The Wants Category

- Cell phone

- Cable

- Internet

- Travel

- Dining Out

- Streaming Services

- Memberships

- Non-essential expenses

How to set up a 30 30 30 10 budget?

Let’s take a quick look at how you set up this budget.

Net Income First

With any budget, the first step is to come up with your monthly after-tax income or net income. For most people, this will be income from their job. This can also include investment returns and income from rental properties. Any form of income that you get regularly is what you want to start with.

Break It Up Into Four Categories

Once you know how much income you have it’s as simple as just multiplying your take-home pay by 0.3 for the first three categories and 0.1 for the wants category.

Let's Look At An Example

If your after-tax income is $5,000 we would split it into:

$5,000 x 0.3 = $1,500 going into housing each month

$5,000 x 0.3 = $1,500 going into savings each month

$5,000 x 0.3 = $1,500 going towards needs each month

$5,000 x 0.1 = $500 going towards wants each month

What Next?

Now that you have looked at how much this budget allows for each category, compare it to how much you are currently spending. In some categories, you may have plenty, but in others, you may have some major cuts you need to make.

The biggest issue for most people when it comes to this budget is going to be in the needs category. You are going to need to find a way to reduce costs so that you can meet the 30% goal. By paying off debt such as an overpriced car, you can make staying within your budget much more manageable.

Pay Off Debt Fast

You will need to pay down the debt fast so that you can get back within the spending goals of the budget. Once you have an emergency fund set up, you will want to transition all extra money into paying off debt. Once the debt is finally paid off, you will have more money for the needs category.

Increase Income

If reducing your living expenses isn’t an option, the only other option is to increase your total income. You can either pick up overtime, grab an extra part-time job, or start a side hustle. If you can increase the amount you make each month, that makes this budget much easier to stick with. Though you don’t want to be working two jobs or overtime forever. So plan accordingly.

Is the 30 30 30 10 budget practical?

Is this budget method practical? The answer to this is it depends. You are going to have to look at your take-home pay and your expenses and be real with yourself. This is a great beginner-friendly budget and should work for anyone who hasn’t dug too deep of a financial hole for themselves.

There are lots of budgeting techniques out there that may be a better fit for you. Don’t be disheartened, the fact that you are here means you are making the first step in the right direction.

If you are looking to start a journey into financial freedom then taking the first step into making a budget is a huge deal. The 30 30 30 10 budget is a great place to start and can help you achieve your financial goals.

Conclusion

The 30 30 30 10 budget is a great beginner-friendly budget for people looking to improve their financial goals. Stop wondering why you don’t have any money left each month and take control of your finances by starting your budget today. You can learn more about budgeting here. If you want help getting started, we offer free resources and advice on our website. Check out our other topics that can lead you to financial freedom!

FAQ

What is a zero-based budget?

A zero-based budget is a method of budgeting all your expenses and income that starts at zero. This means everything you make, save, and spend needs to be accounted for each month. You need to assign every dollar earned or saved and factor in those realistic expenses you have throughout the year too.

Zero-based budgeting might sound daunting, but the key is often just planning so you don’t feel overwhelmed each month. After all, what’s worse than spending money on bills you weren’t expecting?

What is a percentage-based budget?

A percentage-based budgeting system works by allocating a certain percentage from every dollar you earn towards different spending items. The amount of each percentage depends on what you prioritize and need most.

Whatever percentages you decide ultimately get assigned and tracked as part of your overall budget. Having a straightforward way to track income & expenses helps keep the information organized and guilt-free if something doesn’t fit into your overall plan – after all it’s just percentages!

With this type of budgeting, you can do things like consistently save X% each month or increase spending in areas as needed as long as everything else is still moved around accordingly.

Percentage-based budgets are amazing when used to their full potential because they provide clarity on where the money goes before it disappears.

Common percentage-based budgets include

- 50 30 20 budget

- 30 30 30 10 budget

- 60 30 10 budget

Do budgets use pre or post-tax income?

Generally speaking, most budgeting is done using post-tax or net income, meaning any taxes and deductions are taken out beforehand. This simplifies the process since calculations are already completed for you and lets you focus on what matters—figuring out where best to allocate funds.