How much do I need to retire?

Retirement can be a scary time for many Americans. Most people are behind with preparing for retirement. Our current money culture values an expensive car or house over a well-funded retirement account. Let’s look closer and see How much do I need to retire?

Table of Contents

ToggleThe 80% rule

Most money managers default to the 80% rule for retirement income. The 80% rule says that if you make $80,000 while working, you will need approximately 80% or $64,000 a year in retirement. This number includes all forms of retirement income. Such as your 401k, IRA, pensions, social security, and any other source of income you may have when you enter retirement. This number is different for everyone and depends on what you plan to do during your retirement. If you plan to travel frequently or have a winter home in Florida, 90-100% may be what you need to target for retirement. If you save more than average or go into retirement with no debt, 70% is much more realistic.

How to reduce retirement income needs

Enter retirement with no debt; including the mortgage

The average monthly mortgage payment in the United States is $1,275 a month. By paying off your mortgage before entering retirement, you could reduce your yearly withdrawals by an average of $15,300.

If your retirement account isn’t as “juicy” as you hoped, there are ways to reduce the amount you need going into retirement. If you haven’t looked at my post on How to make a Budget, do that first! Then let’s look at some things that could change your retirement outlook.

Along with your mortgage, other debts should be paid off long before entering retirement. If you are still paying off credit cards when you are about to enter your retirement years, you will put yourself at a real disadvantage. Enter retirement with no extra debt, so you can make the most of your golden years.

Factor in what you currently save each month

If you are currently making 80,000 a year while socking away 10% of your take home pay into a Roth IRA or 401k, you may not need as much as you think. Once you retire, the need for saving for retirement is no longer necessary. You can subtract some of the $5,000 to $10,000 from the $64,000 you had planned for post-retirement income. If you consider yourself a “super saver” and have been living off only 50% of your take home pay for years, what makes you think that will change once you retire? All that saving may get you into retirement earlier than you thought!

In retirement, there are multiple ways to make your money go further. If you can hold off retiring, you can decrease the amount needed and increase your monthly take home. Each year you hold off retiring will add approximately 2% to your monthly take home. If you also use that year to put more away in your 401k, you could easily double that percentage.

Healthcare costs

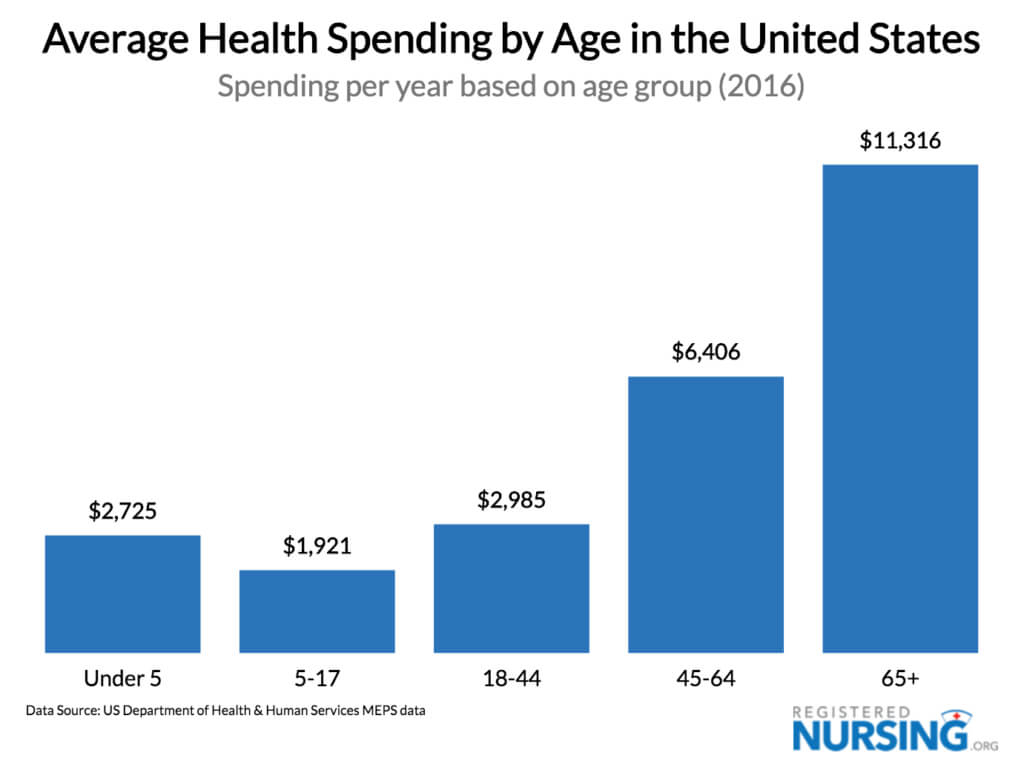

Not all things are cheaper once you get into retirement. Though you planned, you may have forgotten the growing cost of healthcare once you hit retirement age. According to the US department of health, the average annual healthcare costs are $11,316 a year for Americans over the age of 65. Healthcare costs are different for everyone, and can be difficult to estimate in the future. To plan healthcare expenses, it is best to be truthful with yourself and your health risks and plan accordingly. There is a possibility that healthcare costs could push back your retirement date by a year or two.

Final thoughts

Nothing is better than starting your retirement planning as early as possible. This isn’t a possibility for everyone, so making your retirement dollars stretch as far as you can will make a tremendous difference. I suggest sitting down with a financial advisor, going over the numbers, and using what you have learned here and with other research to decide the right retirement date for you.