What is the Average Net Worth by Age

What is the average net worth by age? And more importantly, how does my net worth compare? While there isn’t an exact answer to this question (net worth can vary greatly from person to person), we can take a look at some interesting statistics to get a better idea. So, if you’re curious about where you stand in comparison to your peers, read on!

Table of Contents

ToggleWhat is net worth and how is it calculated?

What is net worth and why is it important

Net worth is a calculation that measures the value of all your assets minus any debts and liabilities you may have. In other words, it’s a snapshot of your financial health at a given moment in time. And while it’s not necessarily the only thing when it comes to gauging your financial well-being, it can give you a good idea of where you stand financially and whether or not you’re on track to reach your long-term financial goals.

While net worth isn’t everything, it is a good starting point for measuring your financial health. And if you’re looking to make some changes in your financial life, knowing your net worth can be a helpful first step in getting there.

How to calculate your net worth

There are a few different ways to calculate your net worth, but the most common method is to simply add up the total value of all your assets (e.g., savings accounts, investments, real estate) and subtract any debts and liabilities you may have (e.g., credit card debt, student loans, mortgage). This will give you your net worth figure.

Assets – Liabilities = Net Worth

Factors that can affect your net worth

Several factors can affect your net worth. One of the most important is your income. The more money you make, the higher your net worth can be. This is not to say lower earners can’t have a competitive net worth.

Another important factor is your savings rate. The more you save, the faster your net worth will grow. However, your savings rate is also affected by your income. If you make a high income but have a low savings rate, your net worth will still be lower than someone with a lower income but a higher savings rate.

Another factor that can affect your net worth is your investment strategy. If you invest too conservatively at a young age you could be left behind. The same goes with an aggressive investment strategy as you near retirement, leaving your large nest egg at risk of a market downturn.

Finally, debt can also affect your net worth. High levels of debt can reduce your net worth, and also leave you with less to save and invest. It’s best to keep your debt as low as possible for your net worth’s sake!

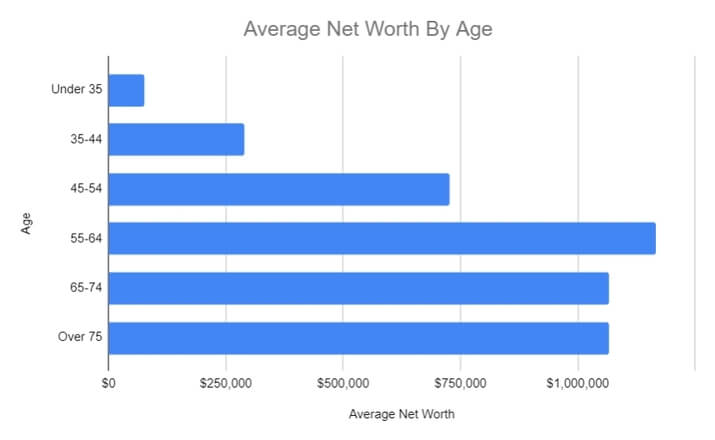

The Average American Net Worth

When looking at the average net worth by age you may be very surprised, just as I was. As someone who takes saving very seriously, I was shocked to see I wasn’t as far ahead of the average American as I had hoped.

When you take into consideration the ultra-wealthy this throws the average off by quite a bit. This is why you shouldn’t be comparing yourself to the average but instead looking at the median net worth. This will give you a better idea of where you stand in comparison.

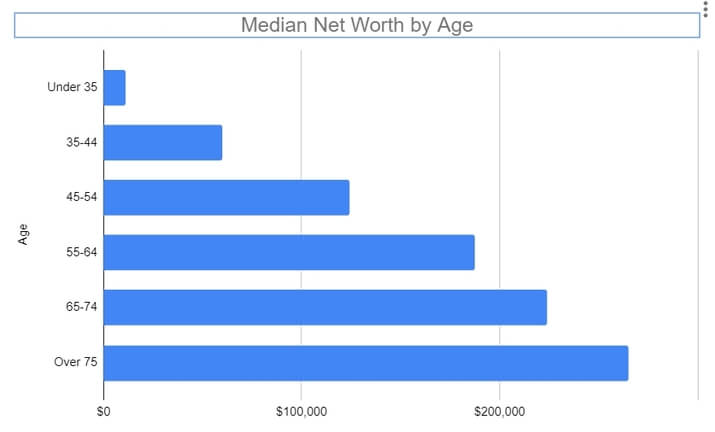

Median Net Worth by Age

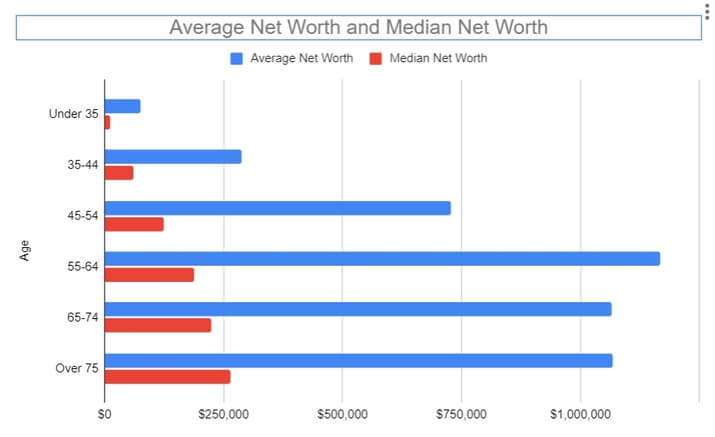

Here is a chart comparing Average Net Worth vs Median Net Worth.

Now not all is good because the median net worth is not exactly an admirable goal if wealth creation is what you are aiming for! The median net worth of the average American is well below where most people should be setting their target for savings.

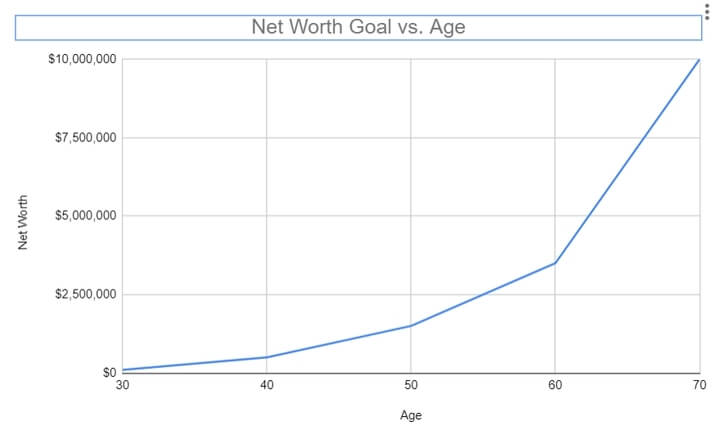

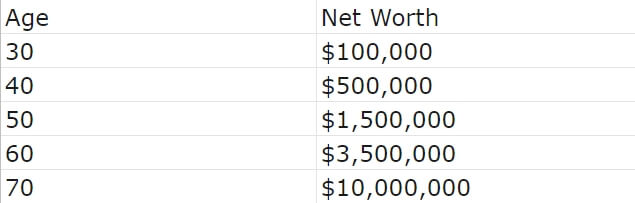

Average Net Worth Goals

The two images above show the same information, one in graph form and the other in table form. Now when you look at these numbers they may seem impossible to reach. And without planning on your part you would be correct that these numbers are impossible to reach. But by starting early and saving as much as possible these goals are very much obtainable.

The number one thing holding people back is not starting early enough. If you can get a good-paying career locked down before 25 and max out your retirement account getting to $100,000 by 30 is a difficult but obtainable target.

By reaching $100,000 by 30 in a retirement account you will be well on your path to financial freedom. Even if reaching multi-millionaire status doesn’t appeal to you, just allowing your money to stay invested will reap amazing benefits.

With the power of compound interest, your investment of $100,000 at the age of 30 could easily be worth $1,000,000! At an annual rate of return of only 8% and invested for 30 years, your investment account would be worth approx $1,000,000 at the age of 60! You may even have enough to retire early.

If this doesn’t excite you about how easy it is to gain financial freedom I don’t know what will! If you are just graduating high school, or recently just obtained your first “real” job, the time is now!

Factors that contribute to changes in net worth over time

The average American’s net worth changes quite a bit throughout their lifetime. Several factors contribute to these changes, including income, savings, investment returns, and debt.

Income

When it comes to net worth, monthly income is just one of many factors to consider. To get a true picture of your financial health, you need to look at your assets and liabilities.

However, monthly income can give you a good idea of how much money you have available to save or invest. It’s also a good indicator of your ability to cover essential expenses like housing, food, and transportation.

If your monthly income is low, it may be difficult to achieve a positive net worth to be used for saving and investing. On the other hand, if your monthly income is high, you’re in a good position to build wealth. While monthly income isn’t the only thing that matters when it comes to net worth, it’s one of the biggest factors in building a high net worth.

Savings rate

How much you save each month has a direct impact on your net worth. Your net worth is the difference between your assets and your liabilities. The more you save each month, the faster you can grow your net worth.

Retirement accounts and your investment portfolio will grow with each deposit you make. And as your savings account balance grows, so does your ability to cover unexpected expenses without going into debt.

The best way to grow your net worth and investment accounts is to start to accumulate assets as early as possible. Retirement accounts have benefits like tax breaks that make them especially attractive for long-term savings goals. But even if retirement is decades away, every little bit you can put into retirement savings will help increase your net worth. So start small and build up from there—your future self will thank you.

When it comes to investment strategies, one size does not fit all. Your investment portfolio should be tailored to your age and risk tolerance. For example, younger investors can afford to take on more risk because they have time to recover from any short-term losses. On the other hand, closer to retirement age, you’ll want to be more conservative approach in order to protect all that money you saved over the decades.

Investment returns are an important part of increasing your average net worth. Over time, compound interest can help your money grow exponentially. That’s why it’s important to start investing early and let your money work for you. Of course, there will be ups and downs along the way, but as long as you stay the course, you should come out ahead over the same time period.

So whatever your age, make sure you have an investment strategy that fits your needs. And don’t be afraid to seek professional help if you need it. After all, your financial future is at stake.

Home equity

For most Americans, their home equity is the largest contributor to their net worth. In fact, according to a recent study, the average homeowner’s net worth is over $200,000 higher than the average renter’s net worth.

Home equity makes up a large portion of Americans’ assets, and as such, it plays a big role in building wealth. There are a few reasons for this. First, homes are typically the most expensive asset that people own. Therefore, even a small increase in the value of a home can have a big impact on net worth.

Second, homes are usually paid off over a long period, which allows the owners to build up equity steadily. And finally, homes are typically one of the most stable investments that people can make. For all these reasons, it’s no wonder that home equity is such an important part of most Americans’ net worth.

Student loan debt

As anyone who has student loan debt knows, it can weigh you down significantly. Not only do you have to make monthly payments, but you also have to contend with interest rates that can add up quickly. And, of course, there’s the knowledge that you’ll be paying off this debt for years to come.

Student loans can also have a major impact on your net worth. Net worth is simply the value of your assets minus your liabilities. So, if you have student loan debt, that’s money that you owe – and it will decrease your net worth.

Of course, this doesn’t mean that you should give up on your dreams of higher education. But it is something to keep in mind as you’re making your financial plans. Student loan debt is a reality for many people – but it doesn’t have to ruin your finances. With careful planning, you can make sure that student loan debt doesn’t take over your life.

Credit card debt

Credit card debt can be a serious problem for consumers. When used wisely, credit cards can offer a convenient way to make purchases and build credit. However, when credit cards are used for everyday expenses, it can be easy to get in over your head.

Credit card interest rates are notoriously high, and it can be easy to make only the minimum payment each month. This can lead to a cycle of debt that can be difficult to break free from.

Additionally, using credit cards for everyday expenses can lead to impulsive spending and make it harder to stick to a budget. For these reasons, it is important to use credit cards wisely and avoid using them for small purchases.

How to increase your net worth over time

Automate your investment savings

If you’re like most people, you probably don’t spend a lot of time thinking about your investment account. But if you want to increase your net worth, it’s important to take a proactive approach to investing.

One of the best ways to do this is to automate your investments. By setting up automatic contributions to your investment account, you can ensure that your money is working for you even when you’re not actively thinking about it.

And over time, this can help you to see a significant increase in your net worth. So if you’re serious about increasing your net worth, consider automating your investments today.

Automate your finances to help you stay on track

For many of us, managing our finances can feel like a full-time job. Between keeping track of our spending, making sure we’re staying within our budget, and saving for our future goals, it’s easy to let our finances get the best of us.

Fortunately, there are several ways to automate our finances and take some of the stress out of managing our money. By setting up automatic payments for our bills and investing in a high-yield savings account, we can take some of the guesswork out of managing our money.

Additionally, using budgeting apps and tracking our spending can help us stay on top of our finances and increase our net worth. By automating our finances, we can take some of the burdens off of ourselves and put our money to work for us.

Review your expenses regularly and find ways to cut back on unnecessary spending

Anyone who has ever tried to stick to a budget knows that it can be a challenge. There always seems to be some unexpected expense that pops up or a tempting purchase that is just too hard to resist.

However, one of the best ways to stay on track with your finances is to review your budget regularly. This will help you to identify any areas where you are spending more than you need to. For example, you may find that you are spending too much on eating out or on subscription services that you never use.

By cutting out these unnecessary expenses, you can free up more money to put toward your savings or other financial goals. So if you want to get a better handle on your finances, make sure to review your budget from time to time.

Pay off high-interest debt as quickly as possible

If you’re like most people, you probably have some form of high-interest debt. Whether it’s a personal loan, credit card debt, or medical debt, interest rates can quickly add up, making it difficult to get ahead. The good news is that there are some simple steps you can take to pay off your high-interest debt quickly and free up money to increase your net worth.

First, make a list of all your debts and their interest rates. This will help you prioritize which debts to pay off first. Then, create a budget and make sure you’re staying within your means. It’s also important to continue making all your minimum payments on time so you don’t damage your credit score.

Once you’ve created a budget, start focusing on paying off your debt with the lowest balance first. You may consider paying off the highest interest first, but that usually isn’t the best option. It is better to pay off lower debts first gaining a boost of confidence and also being able to roll that payment over to the next debt faster.

People who focus on paying debt off based on interest rates usually get “burnt out” and tend to stop before getting too far. By starting with the lowest amount and making headway quickly, you will be much more likely to stay focused.

Once you have paid off all of your debt, it is time to then pivot and use your new-found income for saving and investing. Don’t fall into the trap of spending and getting yourself back into debt. Avoid debt at all costs as it is the enemy of wealth creation.

Tips for saving money and growing your wealth

When it comes to personal finance, a budget is essential. By keeping track of your income and expenditures, you can ensure that your money is being used in the most efficient way possible. However, a budget is not just about cutting back on unnecessary spending. It is also about setting aside money each month to grow your wealth.

By investing in a savings account or mutual fund, you can watch your money grow over time. In addition, you can use your budget to set aside funds for major purchases, such as a house or car. By making a budget and sticking to it, you can slowly but surely build up your savings and achieve financial security.

Invest in yourself by taking courses and learning new skills

It has been famously said that the two most important days in a person’s life are the day we are born and the day we figure out why we are alive. Once we attain an understanding of the role we play in the world we can begin to invest in ourselves, which will lead to an increase in both life satisfaction and possibly your net worth!

One of the best ways to invest in ourselves is by increasing our knowledge. This not only makes us more well-rounded and interesting people, but it also gives us the ability to take on new challenges and opportunities.

Additionally, learning new skills can help us earn more money. So if you’re looking for ways to improve your life satisfaction along with your net worth, be sure to invest in yourself through any form of education.

If you’re looking for other ways to be more frugal, my last blog post is a great place to start. In it, I explore some simple but effective ways to focus on building personal capital while also enjoying more time with family.

For example, I recommend setting up a budget and tracking your spending so you can see where your money is going. I also suggest ways to cut back on unnecessary expenses, like eating out or buying new clothes.

And finally, I talk about how important it is to focus on experiences rather than things. By following these tips, you can save money and improve your financial situation without feeling like you’re depriving yourself. So check out my post and see how you can start being more frugal today!

Final thoughts

We’ve outlined a few steps that, if followed, should help you increase your net worth and secure your financial future. The most important thing is to start saving as early as possible. If you can manage to reach the $100,000 mark by the time you turn 30, you will be in great shape for retirement. But it’s not just about amassing a large sum of money – it’s also important to invest regularly and make sure your expenses are manageable. Finally, automate your finances so that you have less opportunity to spend impulsively or fall into debt. These tips are easier said than done, but with some effort and discipline, you can achieve great things. Are you ready to get started?

One Comment