Building Wealth in 2022

Ask Yourself an Important Question

A question that not enough people ask themselves is How do I build wealth? Building wealth is a lifetime journey. The younger we start building wealth the easier it can be. Sadly many young adults find themselves heading in the wrong direction; building debt instead of wealth. With a few simple steps building, wealth can be something anyone is capable of.

Table of Contents

TogglePay Down Debt

If you owe money to someone else then none of “your money” actually belongs to you. The fastest way to keep from building your own wealth is by building someone elses… aka debt! It is acceptable to split your debt between so-called “good debt” and “bad debt.” Good debt is any debt that is on an investment such as your mortgage or business loans. Bad debt is pretty much everything else. This includes credit cards, vehicles, trailers, and any other debts on its that depreciate in value.

Goal number one is to remove all bad debt from your life. The fastest way to remove bad debt is to sell whatever it is that you owe money on. If your family doesn’t “need” a boat… selling seems like a great option. Also selling items you haven’t used for a while and using the money to pay down debt is also a viable choice.

Once you are left with all the remaining debt, the next step is to pay the bad debt off as quickly as possible. There are usually two schools of thought when it comes to paying off debt. The debt snowball crowd and the highest interest rate crowd. If you are unfamiliar with these methods let’s take a quick look at each.

The debt snowball is paying the minimum on all your debts and using all of your excess money to pay off the lowest dollar amount debt first. Once you pay the lowest debt off you move on to the next lowest using all the money from the previous debt. This will create a snowballing effect, with the added benefit of seeing progress quickly. You can usually pay off your first few debts within a few months and that will give you the motivation to continue on. The downside is if you are not basing your payoff on interest rates you could be going backward with some of your debt.

Paying off high-interest rates first seems to make sense to most people. If someone is charging you more you should pay them back first. This is exactly what the high-interest rate crowd believes as well. Pay the minimum on all your debts and use all excess money on your highest interest rate until you are finished laying it off. Next, choose the next highest interest rate and continue until all debt is paid off. The downside to this is if your highest interest rate is your auto loan for, let’s say $25,000, you could be paying off your first debt for a few years and run out of steam before making much progress.

I find myself somewhere in the middle. I find paying off small debts first to get going makes the most sense. Then once you have more cash free you can divide your last few debts down by a higher interest rate. This will allow you to knock those smaller debts down faster and give you the positive feedback you need to keep plugging along.

Reduce Spending

Once you have finally gotten yourself out of bad debt, you can start cutting back on your spending and start saving more. If you are spending more money on wants than you are saving, then building wealth will be virtually impossible for you. The best way to start spending less is to develop a budget and stick with it. There are many tools online on how to make a budget. Check out this article I wrote on how to develop a budget, and tips to put it into action.

Another great idea that I have suggested for people, with some success, is finding a sponsor to help curb your spending. Find someone who you trust and respect, and ask them to help you become a better saver. They will be a person you can contact any time you are making a purchase that you would consider a “want.” It is best to choose a person that isn’t afraid to tell you no. By training yourself to look at the positives and negatives of big purchases, you will start to develop the skills to cut out unnecessary spending in your life.

Save Extra Money

Now that you aren’t spending like you were before, what should we do with that money? The answer is very easy… save it! Under a mattress, in a savings account, or bury it in the backyard, I don’t care… just put it somewhere you won’t use it on frivolous purchases. Once you work hard and save enough you will start to like the idea of the money more than the stuff it buys. This is the motivation I use to keep myself frugal. If you spend 6 months saving up $5,000 you won’t be as quick to spend that as you are, let’s say, the tax return that you received in one trip to the accountant.

Another trick that I use to save money is to have two separate accounts. One of the accounts is for my spending money and the other is for my savings. I have my checks and debit card attached to my checking account but no way to directly pull money from my savings. Of course, I want to be able to get access to my savings quickly but not too quickly. If I have to transfer the money electronically from one account to another, that can take a few days. In those few days, while I wait, I usually am less excited about the item and can more easily talk myself out of the purchase.

Invest Your Money

Now that you are a super saver and have a nice chunk of change saved, what should we do with our money to build wealth? The key to wealth building is an investment. Without investing your money will get eaten up by inflation. Everyone knows $1000 doesn’t buy today what it did 10 years ago, and we need to protect ourselves. There are many investment opportunities available today, but the one I will focus on is the stock market.

The stock market sounds scary to most new investors. This is mostly because stories of the stock market crashes are talked about for decades, but the market grinding higher over the years is boring. The secret to investing is to invest for the long term. The stock market is an emotional rollercoaster for day traders, but investing for the long term can take most of the emotion out of the market. I am unable to suggest specific investments, but there is a mountain of information available on what stocks and ETFs are worth buying. Do your due diligence and know the company you are investing in.

Another option is investing directly into building your own business. Matthew from MotoNation explains that a part of his investment strategy he will put 10% of his savings into either a new business idea or an existing online business to help grow this income. These businesses generate income which can increase his ongoing savings and can be treated as an asset which can be sold in the future for profit.

Compound Interest

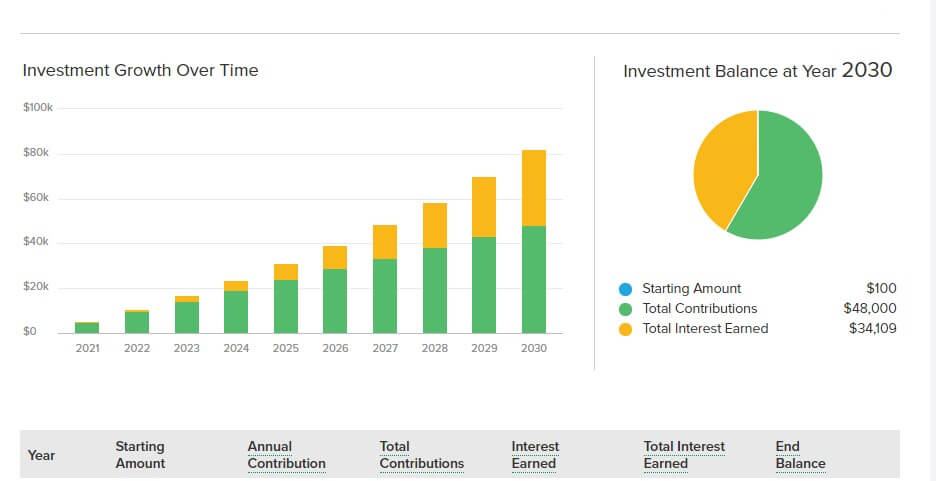

The real key to building wealth is using your money to work for you. When you go into debt, you are allowing the banks to use your money to build wealth for them. If you can turn this around you can put the wealth-building potential in your corner. By building your nest egg through routine saving and reinvesting your profits, you will start to see your personal savings grow much faster than you ever thought possible. Look at the graph below showing what investing a small amount each month can grow into in just a few years.

This is showing what putting a typical car payment away over 10 years can grow into. Investing $400 a month and averaging a 10% return over that time will net you approx $82,209. That is a lot of cash to have on hand and could really change your life if you were to use it as a downpayment on a new home. Now imagine what you will be able to do when you factor in all the other money you freed up, and how quickly you can generate life-changing wealth!

I would like to thank you for the efforts you have put in penning this blog. I’m hoping to check out the same high-grade blog posts by you later on as well. In truth, your creative writing abilities has inspired me to get my very own site now 😉

Thanks for your blog, nice to read. Do not stop.